For businesses operating in Africa, managing cross-border foreign exchange (FX) has become a key part of growth strategy. Currency fluctuations need to be taken into account, whether your business is engaging in international trade or running operations in multiple countries.

In this article, we will explore the intricacies of FX operations in Africa, sharing the learnings AZA Finance has gathered after operating in these markets for more than 11 years. Here is what businesses that regularly engage in international transactions should know about African FX.

We’ll cover:

Strategies for Effective Cross-Border FX Management

The Landscape of African FX

Market Variability & Liquidity Needs

The Role of the U.S. Dollar

The dollar remains the dominant currency in international transactions in Africa. Why is this the case? Most countries rely on the U.S. dollar to pay foreign debts and purchase many essential goods and services. For instance, when governments purchase vaccines from other nations, they will most likely pay for these in dollars.

Additionally, over 80% of African cross-border payment transactions must be routed offshore for clearing and settlement by banks outside the continent. Consequently, intra-Africa trade is at about 16% of global trade.

This article by The Conversation provides a detailed explanation on why dollar shortages happen in African countries. This scarcity has led to increased market volatility, directly impacting businesses that rely on regular cross-border transactions.

Our CEO, Elizabeth Rossiello, captured the problem well for CNBC earlier this year. “Cross-border payments still cost African and African-based businesses too much. African businesses shouldn’t have such a high price (in time or fees) to move into other African or G20 currencies or to make transfers across the continent or into Europe. Yet, they do.”

Varying Exchange Rates

In some African countries, a significant gap exists between official exchange rates and market rates. Countries most affected by this include Ghana, Nigeria, Zimbabwe, and several other West African nations.

This is not the case in East Africa, for instance, where there will be a Bureau de Change (BDC) at hand to offer this retail service. BDCs are licensed by central banks and set their own rates within the central banks’ indicative rates.

Forex shortages and local currency volatility played a big part in the rise of this parallel economy. Governments are doing their best to respond to the circumstances that led to this in the first place. Some examples of measures taken:

- Currency devaluation: For instance, The Reserve Bank of Zimbabwe (RBZ) devalued its currency (ZiG) by 43% in September 2024 to align with market rates. This took the currency from 13.56 ZiG to 24.4 ZiG to the dollar.

- Floating exchange rates: An example here is Ethiopia, which moved towards floating exchange rates to reduce the gap between official and parallel markets while attracting an IMF deal. The Ethiopian Birr was always strong and stable pre-COVID, valued at around 30 ETB to the dollar. However, in the past four years, it has seen several adjustments reaching 57 ETB to the dollar by July 2024. It currently stands at 119 ETB.

- Collaboration with international financial institutions: Countries like Nigeria and Ethiopia are working with the IMF to implement reforms and improve forex supply.

While the black market provides short-term solutions, it poses huge challenges for African economies eventually. In addition to contributing to currency instability, it complicates economic planning among other challenges.

Limitations for SMEs

SMEs are key to driving economic growth in Africa, but they encounter many challenges in accessing new markets, top of which are FX related.

“Small businesses in Africa often pay nearly 200% more than larger businesses to clear transactions through formal channels, and many transactions are conducted via cash as opposed to through formal payment channels,” said our CEO Elizabeth Rossiello to the World Economic Forum.

Formal channels tend to distribute the available liquidity to the largest companies, leaving SMEs to find FX through other channels that tend to be more expensive or dubious.

The Role of Mobile Money

While mobile money has been a great success in Africa, the cross-border aspect of it is not well-expanded. Even one of the largest mobile money companies only launched individual cross border money transfers in 2018.

Africa has more than 171 options for mobile-money wallets, but most can’t work with each other, even within the same country. There are more than 1,000 banks and over a dozen card networks across the 55 countries, but little interoperability makes for a fragmented space. For businesses expanding to the continent from, say, Europe, the difficulty in sending funds can hamstring their operations, especially if they are used to the ease of sending euros across from one country’s IBAN to another.

Despite its monumental growth, with remittances to mobile money peaking to almost $29 billion in 2023, many international merchants do not accept mobile money payments. Most online purchases for goods and services are done via cards like in the West. This limits the customer audience for a business operating or expanding to Africa if they can’t accept mobile money for payments.

Trends Shaping African FX

African FinTech Collaborations

The adoption of financial technologies, including blockchain and AI, in FX operations is on the rise, leading to the growth of cross-border payment flows year-on-year. Fintechs in the continent have built the rails needed to sustain new types of fund flows. Expect to see even more growth in remittances, mobile money, and cryptocurrency payments.

Legacy infrastructure from a decade ago could not make this growth happen. The new technical infrastructure built by fintechs in partnership with the incumbent banks has made this possible. Fintechs are also now operating under the banking licences of partner banks. This collaboration between fintechs and banks is improving the cross-border FX in Africa.

Regulatory Advancements

Keep an eye on evolving regulations. Indeed, it is due to regulatory approval that so many fintech and bank collaborations have been successful in the last few years. Countries like South Africa, Nigeria, and Kenya are at the forefront of establishing clearer frameworks for fintechs and banks. Even as they actively deal with the FX challenges, they are always working with industry players to introduce new licences and frameworks for new players. In doing so, African countries are fostering new international investments and partnerships, enabling the cross-border FX space to thrive.

Best Solutions for African FX

Here is what businesses are doing to streamline their African FX operations.

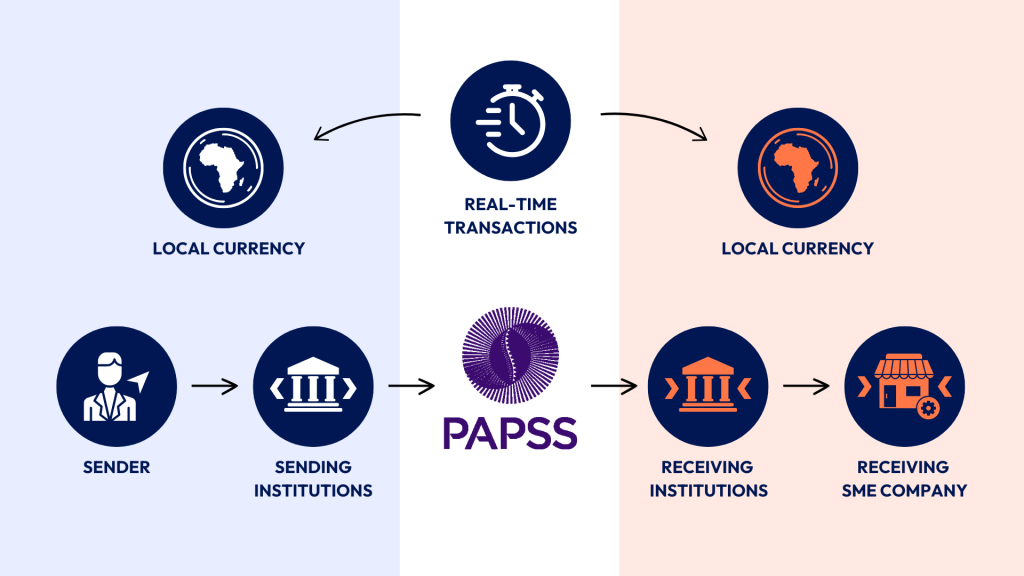

Using PAPSS

The Pan-African Payment and Settlement System (PAPSS) was launched in January 2022 to enable local currency cross-border transactions thus reducing costs which is key to the growth of intra-African payments. PAPSS was birthed out of the African Continental Free Trade Area (AfCFTA) agreement which became operational in 2021 to gradually reduce tariffs on goods and barriers to trade in services.

So far, 14 central banks in Africa and more than 50 commercial banks have joined PAPSS. Read more about its benefits in our previous blog post here.

Using Fintech Platforms

Fintech platforms can give businesses a way to make efficient cross-border payments with plenty of liquidity in the African currencies they need.

For example, the AZA Finance website offers competitive rates for large-volume transactions in major African and G20 currency pairs. Businesses can quickly move funds and exchange African currencies on this platform, lowering their exposure to FX risk.

For businesses that operate specifically in payments, like licensed money transfer operators (MTOs), the AZA Finance API gives them access to multiple local payment methods and instant settlements with its portfolio of currencies.

Using Stablecoins

Stablecoins remain popular in Africa. Stablecoin settlement happens in a few minutes as opposed to the traditional SWIFT systems that can take upwards of a day. Merchants in Africa that have discovered this are increasingly turning to this mode of payment to route their invoice payments in Europe and Asia. In this case, on-ramping and off-ramping is still an important service, since many suppliers do not yet accept stablecoins as payments.

Accounting for approximately 43% of sub-Saharan Africa’s total crypto transaction volume, stablecoins have become a vital tool for businesses looking to hedge against local currency volatility. We have seen this in parts of West and Central Africa where there’s limited access to cross-border banking services.

Strategies for Effective Cross-Border FX Management

Effective cross-border FX management is a must for companies operating in more than one country. It is especially important when:

- A company imports or exports in foreign currencies.

- A company buys or sells in domestic currencies (especially if the intermediary has to change the currency to complete the transaction)

- A company borrows capital from the U.S., Europe or Asia.

- A company has subsidiaries or investments in other countries.

In addition to the innovative solutions like PAPSS, fintech and stablecoins highlighted above, here are some strategies we have adopted ourselves and use daily in our Treasury service for effective cross-border FX management in Africa.

1. Diversify Currency Holdings

Maintaining a diversified currency exposure can help companies reduce FX risk. When a company relies heavily on a single currency, it exposes itself to the risk of fluctuations in that currency. Therefore, companies should aim to maintain a diversified currency exposure.

At AZA Finance, we’re here to provide currency management solutions at the lowest possible rates in the market. You tell what you need and where, and we will settle your payment or transfer in one business day.

2. Monitor Real-Time Market Developments

Regularly monitoring FX market developments to stay informed about potential risks and opportunities allows companies to adjust their operations accordingly. Using platforms like Bloomberg and subscribing to newsletters and daily bank reports ensures your company is abreast with the latest exchange rates, especially in changeable markets.

At AZA Finance, we provide daily rates to customers so that they are equipped with the information to make the right decisions to keep their businesses running efficiently.

3. Consider A More Active FX Strategy

As outlined earlier, there are now fintech products designed specifically for managing cross-border currency operations (and risk). These platforms employ best-in-class financial infrastructure to offer businesses, both big and small, more cost-effective and transparent ways to source and manage FX across borders.

Some solutions include real-time currency conversions, automated currency management and multiple local payment methods. By integrating fintech solutions into your FX strategy, your business can navigate liquidity constraints, access a pool of currency pairs and streamline international transactions.

Indeed, fintech companies like AZA Finance go a step further and include dedicated payments experts and account managers to ensure your business can exchange currencies faster across Africa (talk to us today about this).

Conclusion

Navigating cross-border FX in Africa requires a blend of traditional financial acumen and openness to innovative solutions. By staying informed, diversifying strategies, and leveraging new technologies, businesses can not only survive but thrive in these powerful markets.

At AZA Finance, we also share comprehensive FX insights in our monthly newsletter – you can subscribe below.