Mobile money has changed the financial landscape in Uganda, offering an easy and convenient alternative to the millions who were previously excluded from the formal banking system. According to Statista, in 2022, the number of registered mobile money customers in Uganda amounted to over 34 million and still within that year, the value of mobile money transactions in Uganda was about 8.2 billion U.S. Dollars in the 1st quarter. Due to its widespread adoption, mobile money has become a key means for financial transactions, impacting the lives of individuals and the operations of businesses across the country.

The Ugandan mobile money landscape primarily involves collaboration between telecommunication companies and financial institutions. Through these partnerships, major telcos in the country, including Airtel Uganda, MTN Uganda, Orange Money and others, have been able to promote mobile money services throughout Uganda.

What is Mobile Money?

Mobile money is a service that allows money to be stored and managed through a mobile phone. This digital value is often linked to a mobile phone number instead of a traditional bank account number. Users can transfer and use funds for various purposes, including peer-to-peer (P2P) payments, through SMS-based or application-based transactions. These peer-to-peer money transfers enable users to send and receive money instantly across the country. This has been particularly beneficial for families with members working in different regions, allowing them to support each other without needing physical cash.

The service often includes functionalities like balance checks, money transfers, bill payments, and other financial transactions. Mobile money has simplified the payment of utilities such as electricity, water, and internet services. Many Ugandans also use mobile money to pay school fees, insurance premiums, purchase goods online, and make tax payments.

Depending on the business model, the cash value associated with mobile money is held by the service provider, which can be a Mobile Network Operator (MNO), a financial institution, or a third-party provider. MNOs like MTN and Airtel offer mobile money services directly, while financial institutions and third-party providers may partner with MNOs to facilitate these transactions.

Leveraging the massive adoption of mobile phones, mobile money, also known as MoMo, has become popular because it provides a faster and cheaper means of payment for people who lack access to traditional banking infrastructure, all from the comfort of their mobile phones.

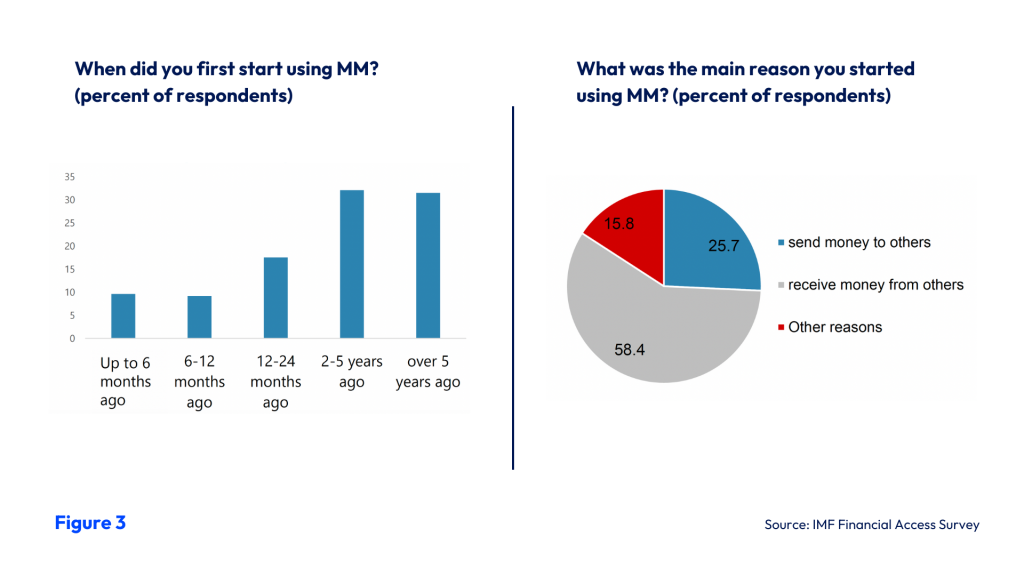

As seen from the figures below, Uganda has experienced consistent growth in mobile money adoption since it was introduced in 2009, and due to this growth, the value of mobile money transactions made up 94 percent of its GDP in 2021, representing one of the highest adoption rates in Sub-Saharan Africa, according to the IMF Financial Access Survey.

![]()

![]()

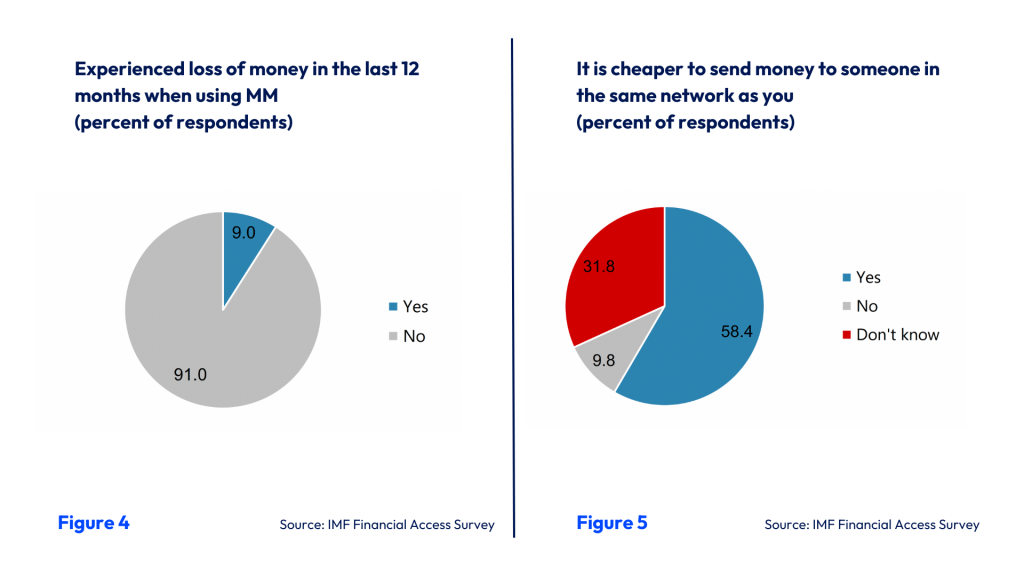

According to the same survey, 81% of respondents have been using mobile money for over a year, with the majority using it for receiving and sending money to others. Additionally, 91% trust that mobile money is safe, as they have not lost money while using the service, and 58.4% believe that sending money to users on the same network is cheaper. See Figures 3–5 below.

As Ugandans’ confidence in mobile money increases, the service has gained significant traction over traditional bank accounts as the 2023 FinScope survey indicates that 66% of Ugandans use mobile money services compared to 13% who use commercial banks. This is a 10% increase from 2018. Its rapid growth is due to its accessibility, convenience, and its role in bridging the gap between the unbanked population and essential financial services, thereby transforming the financial landscape in Uganda.

In Uganda, there are five big mobile money service providers: MTN Mobile Money from MTN, M-Sente from UTL, Airtel Money from Airtel, Warid Pesa from Warid, and Orange Money from Orange Telecom. These platforms offer a range of services, including money transfers, bill payments, savings, and microloans. Recently, MTN and Airtel mobile money made MoKash and Super Saver, respectively, available to help users save small amounts of money and even borrow short-term microloans directly through their mobile phones. The infrastructure supporting mobile money includes a network of agents, robust mobile networks, and regulatory frameworks that ensure secure and efficient transactions.

How Do Mobile Payments Work in Uganda?

In Uganda, mobile payments are typically conducted through USSD codes or mobile applications. Users can deposit money into their mobile wallet or use authorised mobile money agents who operate in nearly every corner of the country. These agents facilitate cash-in and cash-out transactions, helping even those without personal mobile phones, providing a bridge between the mobile money system and physical currency. This money can then be used to pay for goods and services or to transfer funds to other users. In Uganda, there are about 468,476 mobile money agents compared to 27,039 bank agents, highlighting the popularity of mobile payments in the country. With the help of these agents and the extensive mobile network infrastructure, financial services are accessible even in remote areas.

Benefits of Mobile Money in Uganda

Mobile money has brought several benefits to Ugandans including:

-

Bringing Financial Access to More People:

Mobile money helps millions of people who previously didn’t have access to banks, especially in rural areas. It allows them to perform financial transactions without needing a traditional bank account.

-

Making Transactions Easier and More Convenient:

With mobile money, users can handle their financial transactions from anywhere, at any time. This convenience removes the need to visit a physical bank, making it easier for people to manage their money from the comfort of their phones.

-

Helping Small Businesses Grow:

Mobile money has facilitated financial inclusion for small businesses in Uganda by making it easy for them to receive payments and access credit digitally. This has helped businesses operate more smoothly and grow, thereby boosting the local economy.

-

Saving on Transaction Costs:

Compared to the fees that banks charge for transactions, sending mobile money through mobile wallets offers a more cost-effective payment option, especially for transfers between similar network users.

Challenges Ugandans face with mobile money

While mobile money has brought some benefits, there are several challenges that Ugandans encounter such as:

-

Language Barriers:

Many people in rural areas may find it difficult to use mobile money services because the interface is often in English. This can be a problem for those who are not fluent in English or who struggle with reading and understanding the language.

-

Digital Illiteracy:

A lack of familiarity with digital technology can make it hard for some users to access and use mobile money services. Those who are not comfortable with technology may find it challenging to navigate mobile apps or understand how to perform transactions.

-

Unstable Network Connections:

Mobile money services rely on a stable network connection. In areas with poor network coverage, users may experience interruptions or difficulties accessing their mobile money accounts, which can affect the reliability of the service.

-

Security and Authentication Issues:

With mobile money, it may be difficult to protect transaction information, such as PINs, passwords, and other sensitive details exchanged during a transaction. Users may become victims of phishing scams, unauthorised transactions, and agent-related fraud. Additionally, with authentication, the parties involved in the transaction may not be who they claim to be. As a result, there can be security breaches which can lead to fraud and loss of funds particularly among users who may not be familiar with how to protect their accounts.

How Can We Improve Mobile Payment Services?

The future of mobile payments in Uganda looks promising, especially as adoption and integration continue to increase, surpassing traditional banking methods due to their convenience and accessibility. However, there are still ways to improve mobile payment services in Uganda such as:

-

Using local language options as an alternative to English:

MNOs need to consider providing more local languages on mobile money platforms in addition to English as one of the strategies to increase usage among the less literate and rural parts of the population whose proficiency in English is limited. MTN has adopted this strategy with a total of 8 local languages added to their mobile money platform. Airtel incorporates Luganda.

-

Enhancing Security:

To protect users from fraud and unauthorised access, it’s important to implement advanced security measures. This includes stronger encryption for transactions, multi-factor authentication, and regular security updates to safeguard user information and financial transactions.

-

Improving Infrastructure:

Expanding network coverage and upgrading technological infrastructure can help provide stable and reliable mobile money services. This includes investing in better network towers and improving internet connectivity to ensure that users have consistent access to mobile money services.

-

Promoting User Education:

MNOs should continue public awareness campaigns to educate users on how mobile money works, how to use it safely, and how to protect themselves from scams. This can help increase understanding and trust in mobile money services.

How AZA Finance Promotes Efficient Cross-Border Payments with Mobile Payouts in Uganda

During our recently concluded Fintech Fuel Uganda event, we invited key stakeholders from two of the biggest mobile money service providers in Uganda, Airtel Uganda and MTN Uganda, to discuss the current and future state of cross-border payments and the impact of mobile money services in Uganda and across Africa.

Luise Karamagi, Lead of International Money Transfer at Airtel Uganda, expressed optimism about the future of cross-border payments in Africa.

“The future for cross-border payments in Africa is promising because of the huge penetration of phone usage and mobile money services. This can grow more through regional partnerships and integrations and expansion of the mobile corridors,” she stated, highlighting the transformative impact of mobile technology and services on cross-border payments in Uganda and across Africa.

Fatumah Shamim Kavuma from MTN MoMo Uganda also noted the high volume of remittances into Uganda, approximately 5.5 trillion Ugandan Shillings, underscoring the importance of efficient cross-border payments for the economy.

AZA Finance plays a crucial role in this space when it comes to facilitating these cross-border payments and remittances by offering businesses multiple payout options for payments across Africa, including direct payments into mobile wallets and bank accounts.

Through best-in-class payment infrastructure and collaborations with mobile money operators like MTN and Airtel, as well as payment service providers integrated with mobile money, AZA Finance ensures efficient last-mile mobile payouts to beneficiaries in Uganda and across Africa.

Echoing this is Fatimah Gana-Mahmoud, our Head of Sales for West & Central Africa, who highlighted AZA Finance’s success in significantly reducing settlement times from weeks to days, demonstrating the efficiency and reliability we bring to cross-border transactions in Uganda and other African countries.

According to Fatimah, by leveraging partnerships with telecom operators and financial institutions, AZA Finance addresses the key challenges of cross-border payments in Africa such as slow settlement times, high fees, and limited liquidity in African currencies.

With our secure payment services, tailored payment infrastructure for the African market, and access to liquidity in multiple currencies we enhance cross-border payments to Uganda offering mobile payouts for easy and accessible payments.

To find out more about how AZA Finance makes last-mile mobile payouts, click here to speak to a payment expert.